The 2020 global tea market report

Freshly picked tea leaves on a truck on the Sorwathe plantation in Rwanda. Photo courtesy of Barbara Dufrêne

Tea production continues to increase, with robust consumption growth in origin and Muslim countries. However, lagging demand in Western markets, the division between black and green teas, rising production costs, and social responsibility requirements erode company profits, while farm gate prices remain low. Furthermore, adverse weather patterns impact supply and herald climate change. By Barbara Dufrêne

All images courtesy of Barbara Dufrêne

Data and feedback from the United Nations Food & Agriculture Organisation (FAO) Inter Governmental Group (IGG) Tea, located in Rome, Italy, together with the London-based International Tea Committee’s (ITC) Annual Bulletin of Statistics issued in October 2019, offer a thorough overview of the current state of the global tea market. Thus, looking back over the past decade helps identify trends and provide an outlook towards future developments.

Status of Supply and Demand

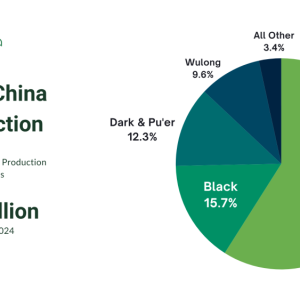

World tea production has increased at an average annual growth rate of 4.7 percent over the past decade to reach 5.89 million tonnes in 2018. This continued growth in global volume was mainly generated by China’s hugely expanded tea output, which has almost doubled since 2009, reaching 2.616 million tonnes in 2018, that is, 44.4 percent of the world’s teas. This massive expansion caters to an unprecedented growth in domestic demand, coming from an ever-growing urban population with more and more disposable income.

Production in India, the world’s second largest tea producer, also shows growth with an output of 1.33 million tonnes in 2018, up by 37 percent since 2009. Output in the two largest tea-exporting countries, Kenya and Sri Lanka, reached 0.49 million tonnes and 0.30 million tonnes respectively in 2018, with Kenya displaying an increase of 57 percent since 2009, whilst Sri Lanka’s tea output, hampered by bad weather conditions and restrictive government rulings, shows growth of only five percent since 2009.

Black teas continue to dominate the market and this dividing line between the black tea and green tea segments remains a major feature of the global tea scene. The traditional auction system, which was introduced during colonial rule in order to secure the supply for British, Dutch and North American consumers is fully focused on black tea. Industrial black tea manufacturing was introduced some 150 years ago in India, Sri Lanka, East Africa and Indonesia for export purposes only. According to Manuja Peiris, chief executive of the ITC, the auction system remains the best way to move important volumes and to cash in the selling price. Being run publicly by appointed staff, the fully transparent system gives good insight into the status of supply and demand and price development.

The auction system may need some overhaul to adopt more flexible procedures and better use of digital methods, noted Joydeep Phukan, the principal officer and secretary of India’s Tea Research Association (TRA). He indicated that investigations are currently ongoing about modernising the Indian auction system, which operates five regional platforms, and moved 41 percent of the total volume of auction-sold black teas in 2018.

El Mamoun Amrouk, the FAO officer in charge of IGG Tea, confirmed these views and underlined that the share of auction sold tea as calculated on the global tea export volume, rose from 61.4 percent in 2009, to 68.6 percent in 2019, which looks like operators continued to approve the system as the best choice. He also said that tea prices were on a downward trend since 2017 but partly recovered in 2019. Talks were ongoing with the Chinese Tea Authorities, to find ways to capture price data for green teas, in order to improve coverage and obtain more insight about global tea sales revenues.

On the other side, there is the highly diversified world of the green teas, which are grown and consumed by the traditional origin tea-producing countries, with China leading, followed by Vietnam, Japan and Korea who have been growing tea for centuries as their peoples’ own heritage cups. In China, which is widely accepted as the cradle of tea cultivation, there are no auction platforms and no agreed grading and quality standards. Thousands of different teas harvested from the many tea regions are displayed on sale in the local towns’ dedicated tea markets, with huge such tea market hubs in Guangzhou/Kanton, Beijing, Chengdu, Shanghai, Wuhan and Kunming, etc.

Trading is carried out in a fully private, person to person manner, with no price/volume disclosure, no transparency and no data. It is a regularly reported fact that for the past few years and with growing demand, tea prices have continued to rise in China. This has now opened a door for India, Sri Lanka and Vietnam to supply some good cups with novelty and a good quality/price ratio, to the Chinese consumers. There is some public auction trading in Japan mainly for sencha green teas, where wholesale companies buy to prepare their blends, but on a very local scale. There are no auctions in Vietnam or Korea.

State of the Global Consumer Markets

Looking at the producing countries, per capita consumption has continued to increase over the past 10 years. This is quite spectacular in China, where the share of the tea output available for export continues to decline, from 22 percent in 2009 down to 14 percent in 2018, and also for India, where only 19 percent of the teas produced in 2018 have remained available for export. One can also see growth in many other producing countries throughout Asia and Africa, where tea is well promoted among domestic consumers, as a healthy and home-grown cup.

In the main importing markets, one can see that decline continues in the mature, mainly black tea-drinking markets that are Russia and the United Kingdom, where imports have decreased by nine percent and ten percent respectively since 2009. This decline is partly offset by the ongoing growth of tea imports to the USA, where tea consumption continues to rise with an increase of eight percent since 2009. The USA now ranks rank as the world’s number three tea-importing market, with 0.12 million tonnes in 2018. Imports for consumption are also up in Pakistan, where volume has more than doubled since 2009, reaching 0.19 million tonnes in 2018 (mainly black tea). Morocco, the world’s biggest green tea importer, registered an increase of 35 percent with 0.07 million tonnes imported for consumption in 2018.

Contrasting data showed that market patterns continue to fluctuate in line with changing consumer preferences, in particular in the mature Western black tea-drinking markets, where the mainstream/mass market cups continue to be the cheapest cup per serving, compared to coffee, juices, bottled water, and dairy. With this decline becoming a persistent market feature, action was taken to reconquer throat-share and revamp the profile of tea. In the United Kingdom for example, Tetley (owned by Tata GB) offered training and teaching to tea professionals, and Russia launched the Tea Masters Cup.

Forecasts may not look satisfactory though, with Unilever, the world’s leading tea manufacturer, announcing during its fiscal year revenues and earnings report, that it is considering selling its global tea business, which includes the Lipton and PG Tips brand, both of which dominate many Western markets. This declaration, made in January with Unilever also stating that mass market black tea bags have no more future in the West, is shaking up the tea world right now. Over the last few years, Unilever has invested in the premium segment by buying Australia’s T2, the UK’s Pukka Organic Herbal tea brand, and the Tazo brand from Starbucks, thus acknowledging that the premium tea segment had important potential for the future.

Selection of standard mass-market teas. Photo courtesy of Barbara Dufrêne

Training and Education

This ties in fully with many actions undertaken by smaller tea companies and trade associations that have been investing consistently in consumer education and in-depth training of tea professionals in order to promote the fine, premium, specialty and origin teas that mainly come as leaf teas. Such efforts are gradually bringing results, with more science and research becoming available every year. Also, tea forums and conventions are promoting the many origins, botanicals and processes involved in tea, which makes the base of keen and knowledgeable consumers larger every year. Fully aware of the intrinsic and added value of these premium cups, they are happy to reach deep into their pockets for hand-picked, artisanal, organic, single estate and other specialty teas.

There are also tea lovers on the producer side, namely in China, and the overseas Chinese communities in Singapore, Malaysia, Hong Kong, and Taiwan, who will pay extreme prices for rare and special spring picks or very famous aged Puer tea cakes. Premium teas have been ranking high on the official state gift list in China, in the same way as the former tribute teas, which, in the past, were reserved for the Emperor.

Sustainability of Lands and Workers

While tea is becoming more expensive in China, most producing countries express concern about the farm gate price levels, which are too low to allow for sustainable tea growing. This links with the fact that in most producing countries the major share of the tea volume is harvested by smallholders, who deliver the leaf to the factory and have no market access themselves, being the first but least empowered link of the supply chain.

With new areas under tea in China, and in Bangladesh, Zambia, Ethiopia, and Mozambique, where tea is introduced with the focus on poverty eradication, sustainability remains a growing concern. When and where better paid crops become available, farmers will uproot the tea bushes to improve their revenue.

The need to build a platform to take care of smallholders’ interests has become truly urgent. To support and advocate for smallholders, the Confederation of International Tea Smallholders (CITS) was established in 2018. Under the supervision of the FAO IGG Tea, the CITS will be hosted in China’s Sichuan province as a first step, but it is not yet fully operational.

In addition, rural labour is becoming scarce as many ageing farmers see their children moving to the cities, and this means that mechanisation will soon become unavoidable.

Furthermore, changing weather patterns threaten many crops including tea, which makes harvests more unpredictable and threaten farmers’ incomes. Looking towards 2030, an expected increased population and less arable land will also put a strain on the five continents’ available fields, with a preferential allocation to food-crop growing, squeezing the acreage for permanent crops, like fruit trees, vineyards, tea, coffee and cocoa. With such forecasts one can expect to move towards a small top premium market for high quality teas and a mainstream market geared towards extracts, ready-to-drink (RTD) teas and industrially processed cups.

There is clearly a need for more science, more agri-research and international cooperation to cope with these many challenges. All the big producing countries have their Tea Research Institutes (TRI) which compile a wealth of knowledge, data and experience. Increased cooperation will foster progress through cross fertilization. Eventually tea will follow the example of coffee and build more global platforms for more global operations and implementations, such as the recently launched CITS for tea smallholders.

Tea Market Evolves Amid Challenges

Consumption trends remain based on health benefits, convenience, novelty and premiumisation, with the stressed urban consumer on the constant look out for a beverage that picks you up without jitteriness, that supplies hydration and functional benefits together with authentic flavours. Good tea has no need for sugary or creamy calories, thus it is fitting to be the cup/mug or can/bottle of the younger generations. RTD teas, sparkling teas and cold brew teas are on the rise in all the developed markets, with their popularity growing steadily.

According to global market intelligence firm Euromonitor International, the top three cold tea markets today by total RTD volume are China, Japan and the USA, but the trend is spreading fast to many other markets.

Although consumption habits are changing and follow new and diversified patterns, from hot to cold, from black to green tea, from brewed to RTD, tea has positioned itself as a drink that is good for the mind and the body, with a rich cultural background. Also, the strong increase in teas blended with herbals, supplement the functionality of the beverage.

Furthermore, tea is harvested from a bush that absorbs CO2 and is considered a poverty relief crop. Recently, coffee shops in China, India and Korea, as well as in the West, have started to carry some quality teacups in response to consumer demand. This is another move that will foster more choice and open new slots for good cups out of home.

- Barbara Dufrêne is the former secretary general of the European Tea Committee and editor of La Nouvelle du Thé. She may be reached at: b-dufrê[email protected].