The Global Tea Report 2024

Tea Rod at Forest Hill Tea in Sri Lanka. Image: Yumi Nakatsugawa

T&CTJ’s annual Global Tea Report examines how, despite a reverence for tea and an underlying good demand for premium and novelty tea, the continued oversupply of mainstream teas is eroding producer revenue and affecting quality. By Barbara Dufrêne

The preliminary main data for 2023 has just been issued to membership by the International Tea Committee (ITC), and the 25th Plenary Session of the Intergovernmental Group (IGG) on Tea of the UN Food and Agriculture Organization (FAO) recently ended. Tea is thus fully in the focus with all the concerned parties: the farmers who produce the leaf, the factories that process it, those who trade, export, import and ship tea, as well as the packers, the multinationals, medium and small operators, the retailers, and the consumers who buy mass market, traditional, premium or novelty tea.

Considered an agricultural product that provides income to millions of smallholders, in particular in remote rural areas, tea is labelled as a ‘poverty relief crop’, and as such, is instrumental for keeping populations on the lands. Often, these farmers will also grow coffee as well as herbs and spices, which all together can provide a fair income. Although many are living reasonably well off their plot, others have no market access and remain poor. When farmgate prices are not rewarding, the leaf quality inevitably goes down, before a possible switch to other crops.

Whilst the main Western consumer markets in North America and Europe are all entirely addicted to their daily morning cups of tea and/or coffee, the global trade pattern of tea and coffee differs greatly, which may help to understand why tea is most often the cheapest cup on display. The fact is that only a relatively small share of the global tea production – ie, just 26 percent in 2023 – is exported, whilst three quarters are consumed by the home markets, which compares to over two thirds of the global coffee production being exported, and only about 34 percent being consumed domestically. Coffee, therefore, gets much more attention in the West and has been benefitting from intense promotion schemes for decades, giving the product a high cup profile that tea has not been able to access to date.

Aerating Vietnam Snow Shan Tea. Image credit: Vanessa Facenda

A first step towards enhancing the product profile globally may well be the introduction of the annual International Tea Day, which was approved by the UN General Assembly in December 2019 and has since been celebrated on 21 May every year. Following the Covid pandemic, the traditionally observed health benefits of tea are consistently highlighted in both consumer and producer markets, and more research is ongoing to take the issue further. However, despite several attempts to set up an interactive global platform for sharing relevant health related data, no effective steps have been taken towards this key target.

It may be of interest to note that some coffee ‘VIPs’ have been heard saying that tea is so obviously good for peoples’ health, that it does not need any further promotion, whilst coffee has to invest continuously to demonstrate that the cup does not carry any adverse health effects, a statement which does provide food for thought.

Production vs consumption

According to data issued by the London-based ITC, which publishes an Annual Bulletin of Statistics, tea production continues to steadily increase year over year and stands at 6.604 million metric tonnes in 2023, ie, up by 2 percent over 2022, and up by 26 percent over the past ten years. At the same time, consumption continues to lag, with an apparent 2023 consumption tonnage of 6.212 million tonnes, hence a gap of 392,000 tonnes between supply and demand, equivalent to about four times the US tea consumption in 2023. The latest provisional data issued by the ITC to membership show that this gap between world tea supply and world tea absorption was the highest ever in 2023 – bear in mind the trade disruptions due to political conflicts which weigh heavily on traditional consumer market patterns, together with the currently ongoing disruptions of transport logistics, in particular in the Red Sea towards the Suez Canal for supply to continental Europe.

China Chengdu tea market alley. Image credit: Barbara Dufrêne

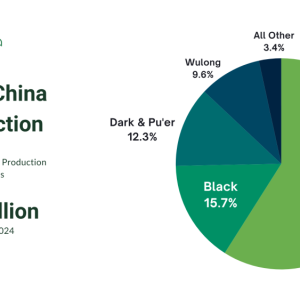

The preliminary data for 2023 shows that there have been no major changes in the main market structure on the supply side, with China remaining the world’s leading producer and continuing to dominate with a production of 3.181 million tonnes, which represents a 49 percent share of the global production. This is quite overwhelming, although domestic consumption absorbs about 88 percent of this production. India holds the second spot with a production tonnage of 1.365 million tonnes, of which less than 17 percent has been available for export. The two giants are followed by the big black tea exporters: Kenya with 353,000 tonnes, Sri Lanka with 251,000 tonnes, Vietnam with 174,000 tonnes, and Indonesia with 125,000 tonnes. Amongst these major tea producers, one must also list Turkey, with a global production of 246,000 tonnes, which is mainly consumed by the domestic market.

The remaining 30 or so countries that produce tea today represent less than ten percent of the global volume, all with volumes less than 100,000 tonnes. This, of course, in no way impacts their quality potential, terroir or specialty tea profile, as they are world respected origins such as Japan, Taiwan, South Korea, Nepal, Malawi and Rwanda – all renowned for their premium quality teas.

Concerning the consumer markets, demand appears to not be fully recovered from the Covid disruptions and is negatively impacted by the various political conflicts that interfere with the traditional trade flows. Thus, the global tonnage of exported teas, which had remained fairly stable, with an average level of around 1.750 million tonnes every year, over the past ten years, has slumped to 1.655 million tonnes in 2023, representing only 26.3 percent of the world production.

The ITC data show a consistent slowdown in the import volumes for all the big consumer markets in 2023 compared to 2022, with the exception of Pakistan, the world’s number one tea importer, keeping the import tonnage at the unchanged level of 236,000 tonnes. All the ‘big players’ show reduced tea import volumes in 2023, namely:

- USA: 104,240 tonnes, -13 percent;

- UK: 83,550 tonnes, -16 percent;

- Russian Federation/CIS: 220,000 tonnes, -5 percent;

- (Rest of) Europe: 129,000 tonnes, -8 percent;

- Central Asian markets: 540,430 tonnes, -5 percent;

- African markets: 344,235 tonnes, -7 percent, amongst which are the two main players (Egypt with 72,000 tonnes, -16 percent and Morocco with 60,000 tonnes, -27 percent) show significant reductions.

Although it is a fact that most producing countries are actively promoting domestic tea consumption, the export markets remain of vital importance to their economy, thus many believe it is urgently necessary to restore the balance between supply and demand. The ITC CEO, Manuja Peiris, recently travelled to East Africa and had many discussions with tea board officials and market operators in Kenya, Rwanda and Malawi. He reported that the Mombasa Tea Auction, the biggest in the world, which handles over 500,000 tonnes of tea per year, is heavily glutted with “unfresh teas,” which remain unsold auction after auction, take up precious storage space and severely obstruct the market.

Indonesia factory leaf variety. Image credit: Barbara Dufrêne

Peiris said he was surprised to learn that many years ago a huge oversupply of coffee had occurred in Brazil, generating such a dramatic price slump that the government decided to act. First, the excess coffee beans were withdrawn from the market and used as fuel for railway engines, replacing fire wood. Next, the government contracted scientific research to find a way to process the beans into a storable and convenient format. It took some time to eliminate the oversupply of green beans and more time to elaborate an attractive soluble coffee extract, but the prices moved up swiftly and some ten years later the Nescafé soluble coffee brand set out to conquer the world. Several decades later Brazil became the world’s number one coffee producer and the number one coffee consuming market (by volume) after intensely promoting quality cups locally. Peiris wonders whether this impressive success story could be adapted to the tea market.

Added value and diversification

There is the huge potential for integrating tea extracts into ready-to-drink (RTD) teas and other cola drinks, which launched in the 1990s in Europe, followed by many evolving RTD launches ever since, despite the drawback of a small sugar content not yet overcome. Instant teas have been extremely successful even before in North America, where brewed iced tea has been the favourite cup for a long time. Chinese and Japanese tea majors have been investing in canned RTD specialty tea and bottled RTD mass market teas for decades and these tea extract-based soft drinks have been spreading widely.

Matcha Organic Japan’s tea field and factory, Shizuoka, Japan. Image credit: Yumi Nakatsugawa

More pricey segments continue to be explored by fine-tuning premium origins and also targeting specific health options. In searching of some more massive innovation, it might be of interest to recall a challenging debate between the former FAO official in charge of IGG Tea, Kaison Chang (who retired in 2018), and some Chinese tea science experts, about a possible “Global Road Safety Campaign,” which promotes small RTD cans or bottles containing a strong and sweetened ‘safe driving tea’. Road safety is a huge issue everywhere, with overtired drivers, not only in China and India, but everywhere in the world. If such bottles of ‘safe driving tea’ were formally approved, labelled as such, and given official support from the UN World Health, the UN FAO, as well as from producer country authorities, their global launch would combine many key assets. With tea extraction factories operating in many producing countries that could cooperate readily in such a Road Safety Campaign, the first result would be the resorption of considerable volumes of leaf.

Looking forward

Whilst there are happy tea farmers, successful tea brands, and thriving tea houses, there are many in the tea industry who are struggling with unrewarding prices, low quality cups, and the lack of global support and high-level genuine product promotion. There are many efforts developed in the consumer markets to enhance product knowledge through tea teaching, tea training, tea tasting competitions, tea awards and more, but there is no global platform and no global structure for providing shared visibility; nor is there a universally supported reference message underlining the goodness of the cup.

Coordinating research about the health benefits of tea would be a great step forward. Establishing a platform to allow direct market access for small producers has been a discussion item on the IGG Tea agenda for several years. There seems to be a growing worry about the lack of an efficient team prepared to take action and follow up the several constructive proposals tabled during the UN FAO IGG Tea plenary meetings, which take place every two years. Whilst they readily take stock, there does not seem to be any follow up action, which is creating true concern.

- Barbara Dufrêne is the former Secretary General of the European Tea Committee and editor of La Nouvelle du Thé. She may be reached at: b-dufrê[email protected].