RTD coffee and tea brands top the BEV50 Brand Index

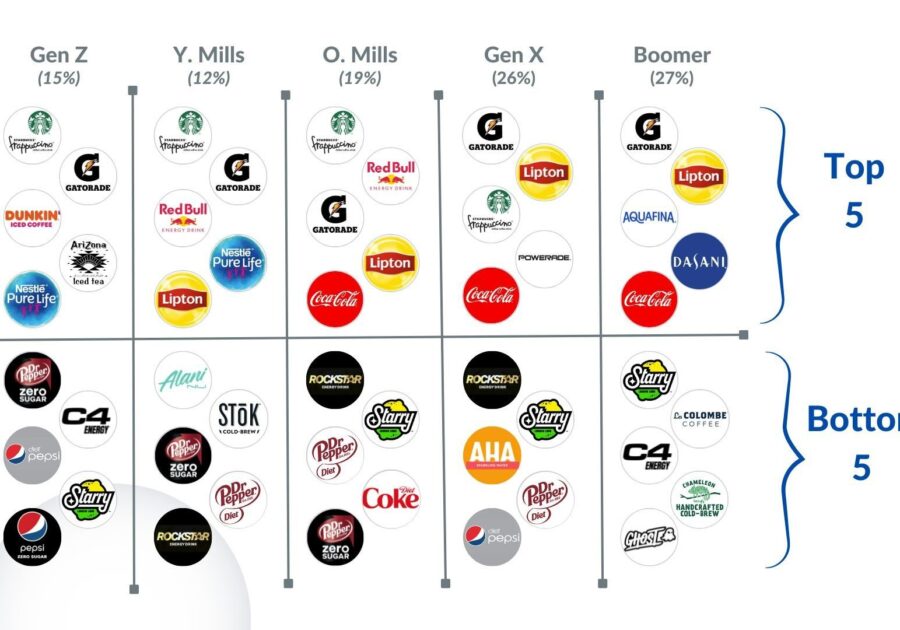

Bev brand preferences among generations graph: Courtesy of Alpha-Diver

Consumers have spoken and Starbucks, Lipton and Dunkin’ ready-to-drink (RTD) products top the list of the 50 most popular brands in the United States. Starbucks Frappuccino, Dunkin’ Iced Coffees and Lipton RTD teas rank among top 10 brands according to the BEV50 Psych-Pulse Brand Strength Index, a new survey that is the first national measure of the psychological drivers of consumer brand behaviour in the soft drink category.

At the category level, the top three performers currently are: RTD coffee, still waters and soft drinks. Brands with the strongest momentum (brand trajectory) include Chameleon Hand-Crafted Cold Brew, PRIME and Electrolit; the weakest in brand momentum include: 7-Up, Sprite and Canada Dry.

The performance of RTD coffee on the list is not unexpected given that 65% of Americans consumed coffee in the past week according to the National Coffee Association’s (NCA) Spring 2023 National Coffee Drinking Trends (NCDT) Survey, with 11% consuming RTD coffee within the past week.

Category laggards – ranking among the bottom three – include enhanced waters, RTD teas and sparkling waters. It is surprising to see the RTD tea category so low on the list given that more than 85% of tea consumed in the US still is either RTD tea or iced tea.

Favoured brands among the youngest and oldest surveyed generations, Gen Z (15% of the US adult gen pop) prefers Starbucks Frappuccino, Dunkin’ Iced Coffee, AriZona Iced Tea, Nestlé PureLife. and Gatorade, while Baby Boomers (27% of US adults) choose Lipton, Aquafina, Dasani, Gatorade, and Coca-Cola.

The Bev50 survey, created by neuro-market research firm Alpha-Diver, is based on 100+ psychological metrics across a representative US population sample. Alpha-Diver is a market research firm that applies neuroscience to better understand marketplace behaviour. The firm’s neuroscientists and strategists work with leading brands, retailers and the Wall Street analyst community to explain, measure, and predict consumer behaviour.

The survey, fielded online (via computer or mobile device) between April and June 2023, among 2,970 respondents, was conducted across eight categories, from multi-billion dollar brands to challengers. There were two waves of 1,500 respondents each, one conducted from 27 April 27 to 2 May, and the second from 2-8 June. The sample is closely matched to US census figures for gender, age, and ethnicity to approximate the general population ages 18-75 as closely as possible.

Fifty-one percent of responders were female, with an average age of 45 and a media income of USD $59,000. Forty-two percent of responders live in suburban settings, 36% in urban areas and 22% in rural communities. The generational breakdown: 15% Gen Z, 32% millennials, 27% Gen Xers, and 27% Baby Boomers. Two-thirds (66%) of responders were White, 12% Hispanic, 14% Black, and 6% Asian/Pacific Islander.

“Our goal was to produce a survey inclusive of all ethnic groups drawn from the key demographic and geographic sectors that explains WHY consumers behave toward brands in the soft drink sector,” said Hunter Thurman, president of Alpha-Diver. “Data drawn from this large sample enabled us to rank the brands according to three dimensions: consumer purchase behaviour, their emotional attachment to brands, and the trajectory of brand usage: increasing, stable or declining. Together this data set provides deeper insights into the beverage sector than previously available.”

Alpha-Diver’s proprietary research methodology breaks down brands by the four leading drivers of consumer behaviour, as well as mapping their sales trajectory, the strength of consumers’ attachment to a brand, and their habituation or routine consumption of beverage brands.

- Experientially-driven brands – providing new sensory discoveries – standouts are: AHA sparkling water, Starry Lemon Lime and LaCroix.

- Rationally-driven brands – practical options – Dasani, Celsius and Aquafina lead.

- Tribally-driven brands –providing a social connection among users – Lipton, Pepsi and Nestlé Pure Life.

- Instinctual – feel good, impulse driven brands – Red Bull, Monster and Mtn Dew, are favourites.

The Bev50 Psych Pulse also includes key data on the five potential barriers to consumer brand choice, including:

- Price: Does the brand offer a good value?

- Time: What must I give up doing to obtain?

- Social: What will others think of me?

- Emotional: Will I be disappointed by the beverage?

- Physical: How will dinking this beverage make me feel?

Consumers have a strong emotional connection to their coffee and tea brands. Currently, the RTD category, within both coffee and tea, is where the most innovation is taking place so its inclusion on the top 50 brand list makes sense. RTD brands are continually meeting consumer demand for new flavours, organic and natural ingredients, unsweetened/less sweetened, lower caffeine/caffeine free, higher caffeine, functional ingredients, improved packaging — the list goes on. I’m curious to see how the list may differ next year — will the same RTD coffee and tea brands ‘make it’ or will new/younger brands top the list?

- Vanessa L Facenda, editor, Tea & Coffee Trade Journal.

Keep in touch via email: [email protected] Twitter: @TCTradeJournal or LinkedIn: Tea & Coffee Trade Journal

TopicsPeopleOrganisations

Alpha-Diver Dunkin' Donuts Lipton National Coffee Association’s (NCA) starbucks

Regions